.png)

By: The Wespath Team

April 6, 2026

The first quarter of 2026 brought heightened volatility as a war in Iran brought geopolitical risk to the forefront and quickly reshaped market dynamics. Our Q1 Quarterly Investor Letter examines how these forces influenced equities, fixed income and private markets, and how Wespath is navigating uncertainty through diversification, research and risk discipline.

Click here to read the full letter

By Connie Christian, CFA

Manager, Fixed Income

February 9, 2026

Compared to a few years ago, fixed income once again looks like a valuable source of diversification for investors. In the low-coupon world of the last decade, bonds offered little income and meaningful downside risk when rates moved higher. Today, the math is different. Coupons are meaningfully higher, and bonds have a much better ability to cushion portfolios during periods of volatility.

Click here to read the full blog.

By: The Wespath Team

January 5, 2026

Wespath’s latest Quarterly Investor Letter shares how our disciplined approach sought to navigate 2025’s market surprises and position nonprofit investors for long-term success. Explore key insights on AI, economic growth and diversification in a year of opportunity and uncertainty.

Click here to read the full letter

By: Jon Morris

December 22, 2025

With the surge in AI stocks raising questions about how the market reflects broader economic realities, now is the perfect time to revisit this question. In this blog, Wespath’s Jon Morris digs into both historical examples and recent trends to highlight the nuances and explain why the relationship matters for investors—especially in today’s fast-changing landscape

Click here to read the full blog.

By: The Wespath Team

December 15, 2025

As we wrap up the year, our investment team is celebrating the holidays with their own twist on the classic Christmas carol. Instead of partridges and pear trees, here are 12 market takeaways, recommendations, traditions and more to spread holiday cheer and insight!

Click here to read the full blog.

By: Meagan Tenety

November 3, 2025

Proponents of sustainable investing can fall into the trap of making it overly simplistic and missing crucial context. We debunk some of these sustainable investing myths and explains Wespath's approach.

Click here to read the full blog.

By: The Wespath Team

October 2, 2025

Despite sticky inflation and cooling labor data, Q3 delivered robust returns for stocks and bonds. Wespath’s latest Quarterly Investor Letter breaks down market performance, Fed policy shifts and other key headlines. CIO Johara Farhadieh and the investment team also highlight our latest fund launch, the release of our Sustainable Investment Report and more news from inside Wespath.

Click here to read the full letter

By: Hoa Quach and Andrew Steedman

September 10, 2025

Wespath is expanding its investment lineup with the International Equity Index Fund – I Series (IEIF-I), a passively managed fund designed to meet the evolving needs of the mission-driven nonprofit organizations we serve. In this blog, Hoa Quach (Director, Public Markets) and Andrew Steedman (Senior Analyst, Investment Management) highlight IEIF-I ahead of its October 1 launch.

Click here to read the full blog.

By: Joe Halwax and Jon Morris

September 2, 2025

While international stocks have been in favor in 2025, U.S. equities have dominated global markets for over a decade. But is this historical outperformance built to last? In our latest blog, Wespath's Joe Halwax and Jon Morris unpack the three key drivers behind the trend and make a compelling case for renewed global diversification.

Click here to read the full blog.

By Joe Halwax CAIA, CIMA

Senior Managing Director, Institutional Investment Services

August 4, 2025

In our latest blog, Wespath's Joe Halwax (Senior Managing Director, Institutional Investment Services) explores how a 10% drop in the U.S. dollar is fueling international equity gains, challenging investor assumptions and redefining diversification strategies.

Click here to read the full blog.

By: Connie Christian and Myles Smith

June 30, 2025

Wespath is adopting the Bloomberg U.S. Aggregate Index as the new benchmark for its Fixed Income Fund and Social Values Choice Bond Fund—enhancing transparency and aligning with industry standards. Learn how this shift empowers investors to better evaluate performance without changing the funds’ core strategies.

Click here to read the full blog.

By Connie Christian, CFA

Manager, Fixed Income

May 27, 2025

From budget negotiations in D.C. to Moody’s downgrading the U.S.’ credit rating, federal government spending has dominated headlines recently. Wespath’s Connie Christian (Manager, Fixed Income) examines the news, sharing both the historical context of the Moody’s downgrade and her perspective on whether it is likely to drive broader uncertainty in U.S. Treasuries.

Click here to read the full blog.

By: Joe Halwax and Raj Khan

May 12, 2025

The prolonged dominance of the United States in global equity markets appears to have hit a pause. From the beginning of the year through the end of April, the S&P 500 Index of U.S. stocks underperformed the MSCI ACWI ex-U.S. Index by more than 16%. Wespath's Joe Halwax and Raj Khan dig into the reasons for this emerging trend and examine whether it's likely to continue.

Click here to read the full blog.

By Johara Farhadieh

Chief Investment Officer (CIO)

April 8, 2025

Wespath CIO Johara Farhadieh reflects on the market volatility brought on by recent tariff announcements and shares a reminder on the enduring principles of long-term investing.

Click here to read the full blog.

By: The Wespath Team

April 3, 2025

Wespath’s quarterly letter for institutional investors provides pertinent market and fund information, plus insights from members of our investment team. For the first quarter of 2025, we explore the pullback in U.S. stocks and the market’s reaction to tariff announcements. We also highlight how Wespath develops custom client portfolios based on the unique needs and objectives of the organizations we serve!

Click here to read the full letter

By: Johara Farhadieh and Joe Halwax

March 24, 2025

The dominance of the Magnificent 7 stocks has led to significant concentration in equity market indexes. Is that effect creating a risk for passive investors? Wespath's Johara Farhadieh and Joe Halwax consider that question, and more, in this blog.

Click here to read the full blog.

By Joe Halwax CAIA, CIMA

Senior Managing Director, Institutional Investment Services

March 10, 2025

We explore how tariffs that were levied against Mexico and Canada, and then paused, could impact the markets, the economy and consumers.

Click here to read the full blog.

By: Johara Farhadieh and Joe Halwax

February 3, 2025

Did you catch the recent headlines about “DeepSeek,” the AI model competing with ChatGPT? Wespath CIO Johara Farhadieh and Managing Director Joe Halwax shared their thoughts on the story—and what it means for Wespath’s investors.

Click here to read the full letter

By: The Wespath Team

January 6, 2025

Wespath’s quarterly letter for institutional investors provides pertinent market and fund information, plus insights from members of our investment team. For the fourth quarter of 2024, we explore the market’s reaction to the U.S. elections and highlight how Wespath’s investment process drove the launch of two new funds.

Click here to read the full letter

By: Fred Huang

December 30, 2024

Baking and investment management produce the best (and tastiest!) results when you have the right mix of ingredients, precision, patience, an understanding of risk and a love of learning.

Click here to read the full blog.

By: Karen Manczko and the Wespath Team

December 16, 2024

As the year comes to a close, it’s natural to reflect on how quickly time seems to pass. The holidays, with all their sparkle and tradition, feel like a moment to pause and take stock—not just of our plans for celebrations, but of the time we’ve invested in what truly matters.

Click here to read the full blog.

By Jake Barnett

November 15, 2024

Recently, Wespath sought out a new investment strategy focused on infrastructure. The process led to a great example of cross-departmental collaboration and asset manager due diligence.

Click here to read the full blog.

By: Karen Manczko

October 11, 2024

As the presidential election draws closer, it's important to understand how such events can influence the markets and why, as long-term investors, we don’t make shifts based on anticipated election outcomes.

Click here to read the full blog.

By: The Wespath Team

October 6, 2024

Wespath’s quarterly letter for institutional investors provides pertinent market and fund information, plus insights from members of our investment team. For the third quarter of 2024, we dive into the Fed's interest rate cut, the potential for renewed interest in small-cap stocks, why it's important to be a patient investor, and more.

Click here to read the full letter

By Johara Farhadieh

Chief Investment Officer (CIO)

September 30, 2024

New Chief Investment Officer Johara Farhadieh cares deeply about mission-driven organizations. Discover how she uses that passion—and her professional experience—to help the people and institutional investors Wespath serves.

Click here to read the full blog.

By Johara Farhadieh

Chief Investment Officer (CIO)

September 23, 2024

New Chief Investment Officer Johara Farhadieh explains why an inclusive approach to hiring asset managers can improve investment returns.

Click here to read the full blog.

By Johara Farhadieh

Chief Investment Officer (CIO)

September 9, 2024

New Chief Investment Officer Johara Farhadieh often talks about how Wespath provides investment excellence. To help you better understand her approach and priorities, Johara explains how asset managers, fees and Wespath staff all play a role in providing investment excellence.

Click here to read the full blog.

By Joe Halwax, CAIA, CIMA

Managing Director, Institutional Investment Services

and Rashed Khan

Director, Portfolio Risk and Analytics

August 16, 2024

Japan’s Nikkei index fell 12.4% on August 4, and then rallied 10% the next day. This volatility, which has been associated with an unwinding of the “yen carry trade,” spilled over to global markets. We explore how these sort of short-term market oscillations impact a long-term U.S.-based investor like Wespath.

Click here to read the full blog.

By Joe Halwax CAIA, CIMA

Managing Director, Institutional Investment Services

While there are very few guarantees in the financial markets, through the first six months of 2024, things are looking fairly positive for investors. The U.S. economy remains resilient, and market leaders like Nvidia keep chugging along. What else is driving returns so far this year? What should we be watching in the coming months? Wespath’s Joe Halwax answers these questions, and more, in our latest blog.

Click here to read the full blog.

By Chirag Acharya

Manager, Sustainable Investment Stewardship

Lucas Schoeppner

Senior Analyst, Sustainable Investment Stewardship

June 17, 2024

Proxy voting refers to casting ballots as a shareholder on corporate governance-related matters at the annual general meetings (AGMs) of the companies in which we invest. All shareholders have the right to participate in AGMs and vote on a variety of corporate governance topics. It’s not typically as dramatic as it’s been depicted on shows like Succession, but it’s no doubt an important element of making our voices heard as an investor.

Click here to read the full blog.

By Andy Hendren

General Secretary and Chief Executive Officer

May 22, 2024

Just a few short weeks after returning home from General Conference, the governing convention and legislative body of The United Methodist Church (UMC), I’m still filled with excitement about Wespath’s support of a renewed, aligned and inclusive Church.

Click here to read the full blog.

By Joe Halwax, CAIA, CIMA

Managing Director, Institutional Investment Services

April 2, 2024

Through the first quarter of 2024, U.S. economic data has remained somewhat strong. U.S. stocks have continued to climb higher, led by growth and technology names. The S&P 500 returned 10.6% in the first quarter, touching a new high of 5,245 at the end of March.

Click here to read the full blog.

By Frank Holsteen

Managing Director, Investment Management

March 18, 2024

If stocks traditionally provide the highest expected returns, why shouldn't you invest your entire portfolio in them? Frank Holsteen, Wespath's Managing Director of Investment Management, examines this question in our latest blog.

Click here to read the full blog.

By Joe Halwax, CAIA, CIMA

Managing Director, Institutional Investment Services

March 4, 2024

Technology-fueled excitement is once again driving a remarkable runup in stocks. But is today’s “Magnificent 7” domination really the same as the dot-com bubble of the early 2000s? In our latest blog, Wespath’s Joe Halwax digs into the characteristics of each era, shares his thoughts on what makes the Magnificent 7 different, and highlights why the real question might be which opportunities will emerge from the rest of the stock market.

Click here to read the full blog.

By Joe Halwax, CAIA, CIMA

Managing Director, Institutional Investment Services

and Rashed Khan

Director, Portfolio Risk and Analytics

January 2, 2024

In our latest blog, Wespath’s Joe Halwax and Raj Khan provide their insights on the top stories from Q4 and 2023 – covering everything from the dominance of the “Magnificent 7” to why continued calls for a recession are starting to sound like a Taylor Swift concert, and much more. Joe and Raj also highlight a few key themes for 2024 to get your New Year started off right!

Click here to read the full blog.

By Joe Halwax, CAIA, CIMA

Managing Director, Institutional Investment Services

and Myles Smith

Investment Analyst

December 18, 2023

We reached out to several Wespath colleagues with the same set of five questions to learn how they make the most of the holidays and to find out about some of their new, exciting experiences in 2023. We hope you enjoy learning more about the people behind the Wespath funds—and maybe get inspired to try something new in the process.

Click here to read the full blog.

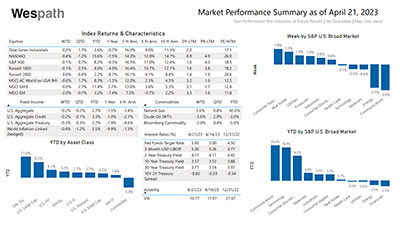

To receive this chart each week via our Wespath Market Update e-mail, please contact our team at [email protected].

We have updated our website with a new look and made it simple to navigate on any device.

We will continue to add more valuable information and features. Please let us know how we are doing.

P.S. For plan sponsors and plan participants, we have a new look for you too. Check out the Wespath Benefits and Investments website.