By Joe Halwax, CAIA, CIMA

Managing Director, Institutional Investment Services

April 3, 2023

| Index | Q1 2023 |

| S&P 500 Index—Gross Return | 7.50% |

| MSCI EAFE Index—Net Return | 8.47% |

| Bloomberg U.S. Aggregate Bond Index | 2.96% |

| Bloomberg Global Aggregate Bond Index | 3.01% |

| Bloomberg Commodity Index—Total Return | -5.36% |

The first quarter began largely positive for global financial markets as moderating inflation remained the dominant theme of the first two months of the year. Nevertheless, in March attention quickly shifted to volatility in the banking industry, as the U.S. witnessed the second- and third-largest bank failures in its history.

We are seeing that as we return to a higher inflation / higher interest rate world, there will be challenges. Simply put, the Fed is in the difficult position of needing to squash inflation while also trying to cause as little damage to the economy, asset prices, and institutions that are hyper rate sensitive like banks.

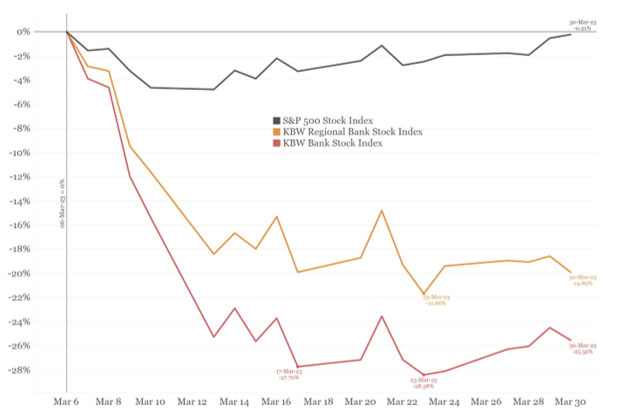

Bank failures create uncertainty, industry volatility

The well-documented collapses of Silicon Valley Bank (SVB) and Signature Bank led to similar uncertainties at U.S.-based First Republic Bank and European financial giant Credit Suisse. Naturally, bank stocks have suffered as a result:

Chart 1: Bank Stock Returns vs. S&P 500 (3/6/23 through 3/30/23)

(Source: Bianco Research, biancoresearch.com, Bloomberg)

It appears that a “worst-case scenario” has been avoided through a combination of government intervention and industry support. Actions from the Fed, Federal Deposit Insurance Corporation (FDIC) and Treasury Department resulted in all SVB and Signature Bank depositors being made whole. First Republic and Credit Suisse were rescued for the time being by other financial institutions, with the latter being acquired by longtime rival UBS.

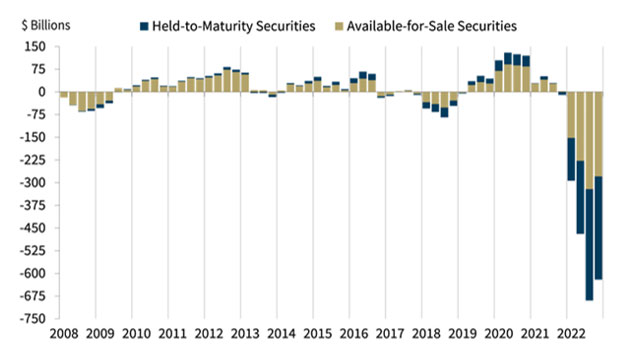

These developments led to heightened attention on bank balance sheets, and analysts have focused on the sharp losses on their books from safe assets like Treasuries and mortgage-backed securities. SVB’s books in particular raised eyebrows, as the California-based bank was foiled in large part because of losses on assets typically deemed as relatively safe, including U.S. Treasury bonds. Following nearly 5% in Fed rate hikes over the past year, the value of these fixed income assets dropped sharply. The following chart shows that this remains an issue for the industry as a whole:

Chart 2: Unrealized Gains or Losses on Investment Securities Held by Banks

(Source: FDIC, Note: “Insured Call Report” filers only)

SVB was a dramatic case, and its failure does appear to be a case of gross mismanagement, as well as the hyper concentration of its client base in growth-oriented technology. However, it’s possible there will be more bank failures given the losses sitting on bank books. Confidence is key for banks, and in this information age where news and rumors spread quickly, banks will be working overtime to show they are capable risk managers.

Still, the industry’s recent headaches are not a repeat of 2008, which stemmed from excessive leverage and consumer loans made with shoddy lending standards. Banks are holding much higher levels of safe assets than prior to the Great Financial Crisis—nearly 35% of U.S. commercial bank assets today are held in cash or U.S. government bonds compared to less than 15% pre-crisis.

Regulators have learned from those past mistakes, too. Governments in the U.S. and Europe were quick to find solutions that protected from financial contagion. For example, the Fed’s new “Bank Term Funding Program” has helped stabilize other banks with liquidity issues.

If you would like more analysis of the banking situation, Wespath Chief Investment Officer Dave Zellner and I collaborated on both a blog post and a video soon after SVB's collapse.

Assuming any further bank industry fallout is limited, focus is expected to return to inflation and central bank tightening.

U.S. inflation moderated to 6.0% year over year in February, as measured by the Consumer Price Index (CPI). That’s down from 6.4% in January and 9.1% just eight months ago. However, the CPI was still up about 0.4% month over month. It would need to be flat or negative to push the year-over-year average back toward the target of 2%. It’s hard to imagine any path to achieving 2% inflation in the next 12 to 18 months without a significant recession that causes negative inflation rates and puts pressure on asset prices.

While inflation remains high, the job market remains strong. The unemployment rate increased modestly to 3.6% in February, up slightly from a 50-year low of 3.4% in January. The last time employment was at 3.4% was 1972. Neil Young’s “Harvest” topped the charts, “The Godfather” was the biggest movie at the box office, “All in the Family” was the most-watched TV show and a gallon of gas cost 36 cents. That was a long time ago.

To make the economic backdrop even more confusing, the Conference Board’s Leading Economic Indicators Index (LEI) fell 0.3% in February, its 11th consecutive decline. It’s now down 5.9% year over year. Historically, when the LEI turns this negative, it’s a reliable indicator of a U.S. recession.

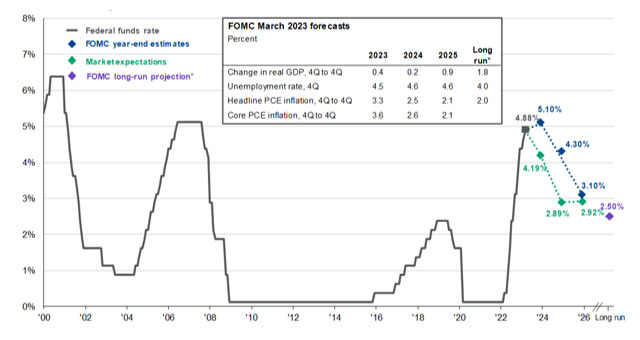

Conflicting economic conditions create a tricky situation for the Fed. The big question now is whether the central bank will pause its rate hikes, or even pivot to cutting rates.

We can probably expect a pause in coming months barring another spike in the inflation data. However, Fed Chair Jerome Powell continues to signal a desire to maintain current levels and not cut in 2023. Meanwhile, futures markets are pricing lower rates much sooner than the Fed is:

Chart 3: Fed Funds Rate Expectations – Federal Open Market Committee vs. Markets

(Source: J.P. Morgan Asset Management, Bloomberg, FactSet, Federal Reserve)

This dichotomy suggests we will continue to see market volatility around inflation data, employment reports and central bank meetings.

U.S. equities rallied on the quarter, with the S&P 500 up 7.5%. The top-performing major U.S. equities index was the Nasdaq at +17.1%, driven by gains at large-cap tech leaders like Nvidia (90.1%), Meta (76.1%) and Tesla (68.4%).

Large-cap and growth-oriented stocks fared better than small caps and value, benefitting from a shift lower in the yield curve and increasing expectations for a Fed pause. As one might expect, financials were the worst performing sector, with the KBW Bank Index down 18.7% on the quarter and nearly all of its losses occurring after the March banking crisis. Financials make up a larger percentage of small-cap and value indexes, which helps explain the underperformance of these indexes.

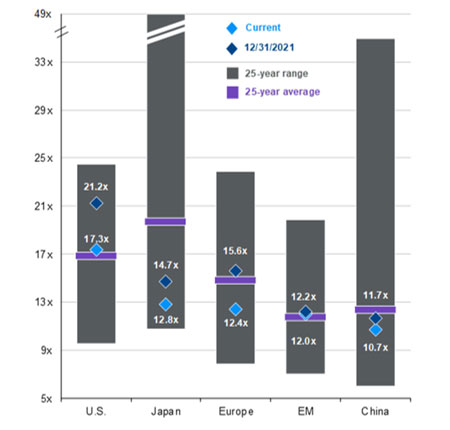

Global stocks also climbed, with the MSCI ACWI ex-U.S. IMI Index up 6.6% and the MSCI Emerging Markets IMI Index up 3.9%. Notably, emerging markets started January strongly, driven by strong performance in China on the theme of continued reopening from COVID restrictions. Still, similar to equities broadly, emerging markets equities have eased amid the bank industry concerns. Emerging markets likely remain compelling for long-term investors because of attractive valuations, improving earnings estimates and a positive outlook for emerging markets currencies. Both emerging markets and other international stocks also look attractive given cheaper valuations:

Chart 4: Global Valuations, Current and 25-year Averages (Forward Price-to-Earnings Ratio)

(Source: J.P. Morgan Asset Management)

Meanwhile, bond markets posted another strong quarter, with the U.S. Aggregate Bond Index up 3.0% amid some of the highest yield curve volatility we have seen in recent history. For example, the U.S. 2-year yield hit a peak over 5% after CPI data and hawkish comments from Powell on March 7—only to fall below 4% a week later after the SVB news. This included the single largest one-day drop for the 2-year yield (roughly 59 basis points) since the 1987 stock market crash.

After falling 17% from Q1 2022 to the end of Q3 2022, the U.S. Aggregate Bond Index has clawed back some 5% as the shift in the yield curve lower in response to both cooling inflation and bank worries. As noted at the end of 2022, bonds remain attractive relative to valuations over the past ten years and will likely remain so barring an unexpected rise in inflation.

There’s no doubt that the news surrounding SVB, Signature Bank, First Republic, Credit Suisse and others was the biggest storyline of the first quarter. Looking ahead, a U.S. debt ceiling debate could start adding to the uncertainties as well. Those are certainly fresh concerns for investors—but beyond that, market movements will likely continue to be driven by inflation and central banks, just as we’ve been discussing for the past 18 months or so. We continue to emphasize the need for patience and discipline while navigating these interesting times. Please contact our team with any questions you may have.

To receive this chart each week via our Wespath Market Update e-mail, please contact our team at [email protected].

We have updated our website with a new look and made it simple to navigate on any device.

We will continue to add more valuable information and features. Please let us know how we are doing.

P.S. For plan sponsors and plan participants, we have a new look for you too. Check out the Wespath Benefits and Investments website.