By Amy Bulger

Director, Private Markets

April 27, 2023

Investors have plenty of options as they look to build diversified investment portfolios that reduce risk, generate long-term returns and help them meet their financial goals. One option that generates much interest and attention is investing in privately held companies, or as its commonly referred to, investing in “private equity.”

Historical data indicates private equity can generate long-term returns above that of public markets, which is attractive to many investors seeking higher yields and returns above a public benchmark (also read: How Alternative Investments Can Benefit Your Diversified Portfolio).

Private equity is an asset class with a long-term investment horizon, many times in excess of 10 years. This makes it a great fit for long-term-focused institutional investors such as endowments and pension plans. These types of organizations typically allocate a significant portion of their assets, from 5% to 15% on average, to private equity investments.1 In fact, some of the larger educational endowments, including Yale and Harvard, are known to allocate a higher percentage to the private equity sector in what is referred to as the “endowment model.”

Another reason why private equity is more attractive to large institutional investors is greater potential to influence company outcomes compared to purchasing stock of a public company. For example, private equity asset managers may take a more active role in the management of a company. Their investment is considered a partnership with the owner(s) of the private company and could include assistance with growing management’s expertise, developing and executing new business plans, and finding new ways to improve operations of the company. These initiatives take time to develop, and as a result, they contribute to private equity’s longer time horizons and illiquid nature.

Traditional Private Equity Funds

The most common type of private equity fund structure is the 10-year, closed-end “Limited Partnership.” The life cycle of these funds plays out in the following steps:

As implied by the name, the goal of these funds is to have exited all investments within the 10-year period. In reality, though, these funds usually take much longer to exit all their investments—sometimes up to 20 years. This extended time horizon can create problems for some investors, particularly those that are seeking liquidity and would like to realize the returns on their investment:

Alternative Structures to the Traditional Closed-End Fund

Common alternatives to the 10-year limited partnership structure include evergreen and open-end funds, which as their names imply, have no termination date and allow for capital to be raised or repaid on an ongoing basis. These funds offer solutions to some of the more common complaints of closed-end funds, including the illiquidity issue mentioned above. Evergreen and open-end funds also create distinct opportunities—because the strategy is not focused on a pre-determined exit date, fund managers can invest in businesses that benefit from more patient capital.

There are, however, some key differences between open-end and evergreen funds. Most importantly, open-end funds typically distribute their proceeds to investors, while evergreen funds are structured to “recycle” distributable proceeds into new investments.

How Evergreen Funds Work

Investors are increasingly recognizing evergreen funds as an attractive solution for maintaining a consistent exposure to the private equity sector without having to continually reinvest distribution proceeds.

The evergreen fund also allows investors to closely control their private equity allocation by offering the opportunity to redeem capital or invest new capital on an ongoing basis. To do this, evergreen fund managers must ensure that there’s enough liquidity in the fund to execute such transactions. This liquidity is achieved by investing some of the fund in assets with shorter durations, such as private credit, which deliver more predictable cash flows and can fund redemptions and reinvestments.

But providing liquidity does pose a risk for the fund manager. For example, if too many investors need to sell their positions in the fund at the same time, it could force the manager to quickly sell assets at below-market prices, which may destabilize the fund. Evergreen funds always have some type of “gating” restrictions to prevent this from happening, meaning they allow only a portion of assets to be redeemed within a set time period. This helps ensure the fund is acting in the best interest of all fund investors, rather than just those seeking to redeem at a certain time.

What This Means for Wespath Institutional Investments (WII)

WII includes an allocation to traditional closed-end private equity and private real estate funds—up to 10%—within our domestic and international equity funds, U.S. Equity Fund – I Series and International Equity Fund – I Series. We value the benefits of diversification and potential for returns above a public market benchmark that these allocations can offer. Plus, by including them within our daily traded equity funds, we mitigate many of the liquidity challenges of traditional closed-end funds on behalf of our investors.

Nevertheless, we recognize that our investors have a wide range of financial goals, some of which may be well served with more direct exposure to private markets. Living into our commitment to serving our investors’ needs, we sought new ways to deliver such exposure within the I Series funds.

This quarter WII launched the Alternative Asset Fund – I Series (AAF-I), a new fund developed in partnership with an industry-leading private markets asset manager. AAF-I is structured like an evergreen fund, seeking to provide investors with adequate liquidity and ongoing alternatives exposure.

Please contact the Institutional Investment Services team (e-mail: [email protected], telephone: 1-847-866-4100) for more information on AAF-I, including requisite qualifications for investing in the fund.

1 Source McKinsey & Company Global Private Markets Review 2022.

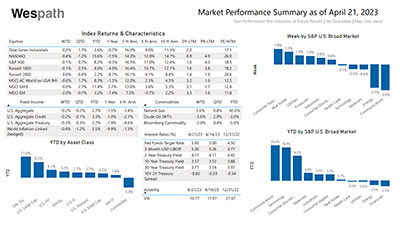

To receive this chart each week via our Wespath Market Update e-mail, please contact our team at [email protected].

We have updated our website with a new look and made it simple to navigate on any device.

We will continue to add more valuable information and features. Please let us know how we are doing.

P.S. For plan sponsors and plan participants, we have a new look for you too. Check out the Wespath Benefits and Investments website.