By: Connie Christian, CFA

(Manager, Fixed Income)

February 9, 2026

Another core tenant of Wespath’s investment philosophy—purposeful diversification—is relevant in today’s environment, as fixed income looks to remind investors about its critical role in a multi-asset portfolio.

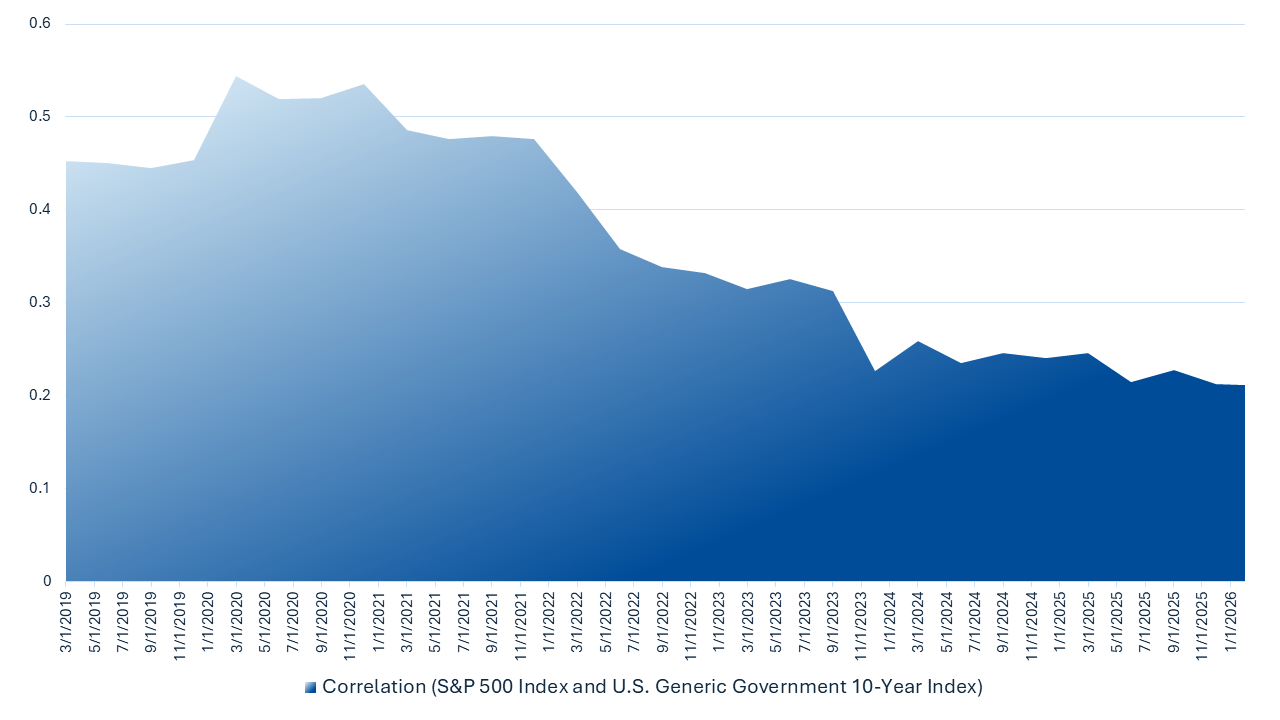

For example, with inflation well off its 2021-2022 highs, the correlation between bonds and equities has begun to normalize, restoring fixed income’s diversification benefit. In fact, the correlation between 10-year U.S. Treasuries and the S&P 500 Index, as shown in the chart below, has been declining for several years:

A lower correlation between stocks and bonds is beneficial for the purposes of diversification, as bonds often serve to reduce risk and provide stability during volatile periods for equities. If in practice stocks and bonds move higher and lower at the same time, this core purpose becomes muted. Correlation peaking during 2020 and 2021 is no coincidence: When there is higher unexpected inflation, interest rates increase and bond prices decrease, and at the same time, rising costs erode corporate profits and put downward pressure on equity valuations. Thus, cooling inflation has helped usher in a return to normalcy in the correlation between stocks and bonds.

Said differently, investors seeking diversification have choices again. Organizations with lower risk tolerance or pools of capital that require more stability no longer need to reach far out on the risk curve to generate income. High-quality bonds can once again do what they are meant to do: provide income, preserve capital and diversify equity risk.

That said, fixed income investing is not without risks. Increased fiscal spending is a meaningful concern, particularly in developed markets where debt levels are already high. Larger deficits can put upward pressure on long-term yields and increase volatility in government bond markets. Geopolitical risks remain elevated, from ongoing conflicts to trade tensions and supply chain realignments, all of which can introduce inflation shocks or sudden risk-off episodes. But these risks argue for humility, diversification and active oversight, not for avoiding fixed income altogether.

Additionally, Wespath’s investment process is designed to help mitigate these risks through disciplined and repeatable oversight. We emphasize purposeful diversification not just across asset classes, but also across sectors, strategies and managers, when investing in fixed income.

Meanwhile, thorough due diligence seeks to evaluate whether underlying managers have the skill, process and resources to deliver on their stated objectives. Clear guardrails help keep the overall fund aligned with its intended structure, while well-defined guidelines and risk controls provide Wespath’s investment managers with the tools and boundaries needed to manage portfolios prudently. Together, these elements create a framework that empowers resilience across a range of market environments and is well suited to support the missions of nonprofit institutional investors.

Subscribe Now!

Interested in more investment content? Be the first to receive our free resources—newsletters, webinars, and updates from our team and industry leaders—designed to help you stay informed and inspired.

Subscribe Now!Ready to Connect with Wespath?

Wespath provides OCIO services and investment management solutions to faith-based organizations, churches and other mission-driven nonprofits. If your organization needs help with policies, endowments or values-aligned investing, we’re here to help.

Contact Us!We have updated our website with a new look and made it simple to navigate on any device.

We will continue to add more valuable information and features. Please let us know how we are doing.

P.S. For plan sponsors and plan participants, we have a new look for you too. Check out the Wespath Benefits and Investments website.