By Jon Strieter

Analyst, Impact Investments

October 26, 2021

In my two plus years at Wespath, I have become increasingly involved in reviewing transactions that are submitted under our longest running impact investment initiative, the Positive Social Purpose (PSP) Lending Program.

Many of you will already be familiar with the PSP Lending Program—it’s our internally managed strategy that invests in loans supporting affordable housing, community development and microfinance. Since 1990, the program has consistently sought to deliver market-rate, risk-adjusted returns to investors while making a positive impact on underserved communities.

I must admit, when I first joined Wespath, I had minimal knowledge about the affordable housing industry and the positive effects it has on individuals and communities in the United States. I’ve enjoyed the “hands on” experience with this type of investing, and I think our participants and institutional investors may be interested in learning more about the program and how the affordable housing business works.

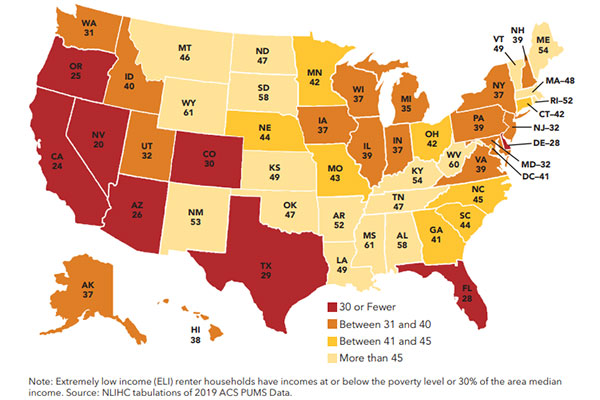

Rental Homes Affordable and Available Per 100 Extremely Low-Income Renter Households By State

Source: https://reports.nlihc.org/sites/default/files/gap/Gap-Report_2021.pdf

Partnering for Success

As I mentioned, the PSP Lending Program’s basic objective is to seek competitive returns while affecting positive impact. The program accomplishes this by collaborating with qualified lending partners—which we refer to as “intermediaries”—and investing in loans that support low- and moderate-income individuals, families and communities.

Most PSP loans finance properties supported under the Low-Income Housing Tax Credit (LIHTC) program. Created in 1986, the LIHTC program is the federal government’s primary tool for supporting the development and preservation of affordable housing across the country. It serves families, veterans, seniors, disabled persons and individuals experiencing homelessness.

Since LIHTC’s establishment, it has supported more than 49,000 projects and 3.34 million units, making it the largest source of affordable housing financing in the United States.1 We are pleased to be a part of this successful history—through the PSP Lending Program, Wespath has financed almost 53,000 housing units through a total investment of nearly $2 billion.2

The LIHTC program is a public-private partnership that offers incentives to affordable housing developers and investors. After receiving a tax credit award under the LIHTC program, developers will typically seek equity investors in the project by selling the tax credits to taxable private investors. Developers earn fees for constructing and managing projects. Tax credit investors, including banks and insurance companies, can claim the tax credits, typically over a ten-year period, and receive a dollar-for-dollar reduction of their annual tax liability.

Oversight Supports Performance

Although LIHTC is a federal tax incentive, state housing agencies are the primary administrators that award tax credits to developers. Each year, states receive a LIHTC allocation that is determined by a formula utilizing each state’s population. State allocating agencies are responsible for annually detailing how they intend to award the tax credits under their published Qualified Allocation Plan (QAP). Each state’s QAP outlines criteria that the state considers when evaluating projects as well as directives that developers must follow to apply for tax credits.

When applying for LIHTC credits, developers are required to provide details about their organization as well as the housing project’s concept, location and financing assumptions. These applications are closely scrutinized, with state agencies considering overall economic and market indicators, the project’s fit within its market area, the financial feasibility of the project, and the background of the developer’s team.

For example, the Illinois Housing Development Authority’s 2022 – 2023 QAP scoring matrix includes six main categories for evaluating project applications: project design and construction, sustainability, community characteristics, development team characteristics, financial characteristics, and policy initiatives. 3

The process for developers to receive LIHTC credits is long and complex. This is also a highly competitive market. The demand for tax credits from developers almost always exceeds the LIHTC allocations available each year.

Because the LIHTC program is so competitive, and because the allocation process is so thorough, only the strongest projects are awarded credits. This means LIHTC projects tend to have the best possible underwriting and oversight, which, in turn, benefits investors like Wespath because these projects typically have low default rates and strong long-term performance.

In other words, the LIHTC program helps Wespath seek out strong investment returns for our stakeholders, while providing safe and affordable rental housing options in local communities. If you are interested in learning more about LIHTC, we recommend this helpful guide from tax consultancy Novogradac.

1 https://www.huduser.gov/portal/datasets/lihtc/property.html

2 Investments in the PSP Lending Program are made through Wespath funds which are available, depending on the nature of the investor and the assets to be invested, through Wespath Benefits and Investments or Wespath Institutional Investments. The information provided relates to the combined investments of all Wespath funds in the PSP Lending Program.

What themes would you like us to cover in future blog posts? Let us know at [email protected]

To receive this chart each week via our Wespath Market Update e-mail, please contact our team at [email protected].

We have updated our website with a new look and made it simple to navigate on any device.

We will continue to add more valuable information and features. Please let us know how we are doing.

P.S. For plan sponsors and plan participants, we have a new look for you too. Check out the Wespath Benefits and Investments website.